Imagine a country that generated, in 2025, more than three quarters of its new electricity from the sun, the wind, and water. That country exists and it is called Brazil. While much of the world is still debating how to reduce dependence on fossil fuels, Brazil enters 2026 in an enviable position: 84.63% of its installed electricity capacity already comes from renewable sources. But like any major transformation, contradictions appear along the way. And they are revealing.

At the same time that data from ANEEL points to a record increase of 9.1 GW of new capacity in 2026, solar energy, which was the star of the past decade, is beginning to stumble due to regulatory problems, lack of transmission infrastructure, and interest rates approaching 15% per year. What is happening to Brazil’s power sector? And where is it headed?

An Energy Mix That Became a Global Benchmark

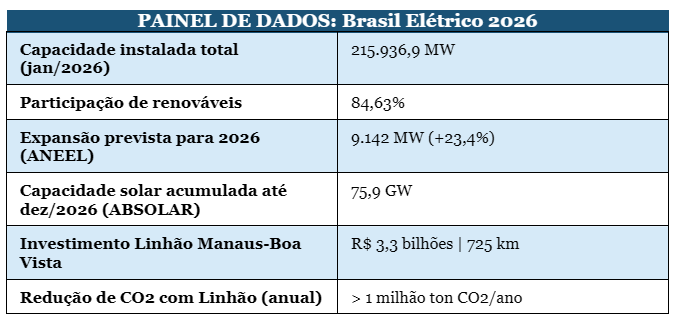

The numbers are indeed impressive. According to data from SIGA (ANEEL’s Generation Information System), on January 1, 2026 Brazil recorded 215,936.9 MW of monitored capacity in centralized power plants. Of this total, 84.63% corresponds to renewable sources such as hydropower, wind, solar, and biomass.

For 2026, ANEEL projects an additional 9,142 MW added to the system, a volume 23.4% higher than the result achieved in 2025, when 7,403.54 MW were added to the national generation fleet. The data comes from ANEEL’s Electricity Generation Supply Expansion Monitoring Report (RALIE).

In 2025, 136 power plants entered commercial operation. The composition of this growth says a lot about where Brazil is heading: 63 solar photovoltaic plants (2,815.84 MW), 43 wind farms (1,825.90 MW), 15 thermoelectric plants (2,505.77 MW), 11 small hydro plants (199.34 MW), and one 50 MW hydropower plant. In other words, renewables accounted for 76% of everything installed that year.

To put these numbers in perspective, 9.1 GW of new capacity is roughly equivalent to the power output of the Itaipu power plant. In a single year. And predominantly from clean sources. In this regard, Brazil has already become a case study for the world.

The Transmission Line That Completed Brazil’s Map

If there is a symbol of what Brazil’s power sector achieved in 2025, it stretches 725 kilometers, includes 1,390 towers, and cost R$3.3 billion. It is the Manaus–Boa Vista Transmission Line, the project that on September 10, 2025 connected Roraima to the National Interconnected System (SIN) and ended decades of energy isolation.

Roraima had been the only Brazilian state still dependent on diesel-fired thermoelectric plants for its electricity supply. Besides being expensive and polluting, these plants left the state vulnerable to frequent blackouts, especially on weekends when demand fluctuated. The situation was so critical that the cost of this system was shared among all Brazilians through the Fuel Consumption Account (CCC).

With the energization of the line, operated by Transnorte Energia (a consortium formed by Alupar with 51% and Eletronorte with 49%), Roraima began receiving clean and renewable electricity from the SIN through a double-circuit 500 kilovolt (kV) line passing through the Eng. Lechuga (AM), Equador, and Boa Vista (RR) substations.

The impacts are multiple. The project will reduce CO₂ emissions by more than 1 million tons per year with the gradual shutdown of thermoelectric plants. It will save more than R$500 million annually in fossil fuel costs for the national system. And it will provide Roraima with an energy capacity roughly four times greater than the state’s current demand, creating conditions for industrial development and even electricity exports to neighboring countries such as Guyana, Suriname, and Venezuela.

The project took nearly fifteen years to move from planning to completion. Auctioned by ANEEL in 2011 with an expected delivery date of 2015, it faced environmental and legal obstacles, particularly due to a 122 km stretch crossing Waimiri-Atroari Indigenous territory. In the end, it was completed at a cost far above the original estimate, but the result is undeniable: Brazil is now one of the few countries in the world with its entire national territory electrically interconnected.

Solar Energy: The Giant with Feet in the Mud

Solar photovoltaic energy was undoubtedly the phenomenon of Brazil’s electricity sector over the past decade. In 2024, the country added 15 GW of new solar capacity, a historic record. But the winds have shifted. According to the ABSOLAR (Brazilian Solar Photovoltaic Energy Association), the country is expected to add only 10.6 GW in 2026, a 7% decline compared to the 11.4 GW added in 2025, which itself already represented a 24% drop compared to the previous year. It will be the second consecutive year of slowdown.

For those following the sector, this retreat is no surprise. It results from a combination of factors that have accumulated over the past two years:

- Uncompensated curtailment: large solar and wind plants have been experiencing generation cuts imposed by the National System Operator (ONS) when the transmission network cannot transport all the energy produced. The issue is that without a consolidated compensation mechanism for the megawatt-hours not delivered, investors lose revenue predictability and hold back new projects.

- Connection denials in distributed generation: small and medium photovoltaic systems installed on rooftops and small properties are facing a growing wave of rejections from distribution companies, which claim the grid lacks the capacity to absorb new generators without causing reverse power flow.

- High cost of capital: with the Selic rate close to 14.75% per year and credit costs for the sector approaching 15%, financing a solar project has become significantly more expensive, compressing margins in an already highly competitive segment.

- Exchange rate and imports: high volatility in the dollar and elevated import taxes on photovoltaic equipment have increased project costs and reduced investor appetite.

The economic impact is significant. ABSOLAR projects R$31.8 billion in solar investments in 2026, a 20.5% drop from the R$40 billion estimated for 2025. Job creation in the sector is also declining: from 396,500 new positions in 2025 to 319,900 in 2026. Tax revenue associated with the solar supply chain is expected to fall from R$13 billion to around R$10.5 billion.

Despite this, photovoltaic capacity will still grow in absolute terms. Brazil is expected to end 2026 with a cumulative solar capacity of 75.9 GW, with 51.8 GW in distributed generation systems (rooftops and small properties) and 24.1 GW in large centralized plants connected to the SIN.

The Transmission Bottleneck: The Achilles’ Heel of the Transition

All this expansion of renewables collides with an uncomfortable reality: the transmission network has not kept pace with the growth of generation. The result is paradoxical. Power plants are ready, sun and wind are available, but the electricity cannot reach consumers because the lines are saturated.

To address this bottleneck, the federal government plans two major transmission auctions in 2026. The first, scheduled for March, is expected to offer around 888 km of new transmission lines across 12 states, with investments of roughly R$5.7 billion. The second auction, planned for the second half of the year, promises to be even larger: more than 3,500 km of lines and investments exceeding R$20 billion.

Additionally, an unprecedented auction in Brazil is scheduled for April: the Capacity Reserve Auction (LRCAP), dedicated exclusively to contracting battery energy storage systems (BESS). Approved by Law 15.269/2025, the auction is considered essential to absorb excess solar and wind generation during peak production hours, storing energy and dispatching it during periods of higher demand. It would be the first Brazilian auction of its kind.

What the Numbers Say About the Future

The Brazil emerging from the 2025–2026 data is contradictory yet dynamic. On one hand, an electricity mix that is already a global benchmark in renewables, with rapid expansion and infrastructure growing at a fast pace. On the other, a solar sector stumbling over regulation, insufficient infrastructure, and the high cost of capital, signaling that growing too quickly without regulatory and network foundations keeping up has consequences.

According to the EPE National Energy Balance 2025, solar and wind sources together already account for 23.7% of the country’s total electricity generation. In 2024, solar generation grew 39.6% while wind advanced 12.4%. Energy consumption is also expected to keep growing at an average rate of 2.1% per year through 2034, driven by economic expansion, extreme heat, and the boom in artificial intelligence data centers choosing Brazil precisely for its clean and relatively inexpensive energy mix.

The response to the sector’s current challenges is being built on multiple fronts: expansion of transmission infrastructure, regulation of energy storage, compensation mechanisms for curtailment, and modernization of connection rules for distributed generation. It is not a simple solution. But the path is already being drawn.

A Country in Real Transformation

Brazil’s power sector is undergoing in 2026 a structural transformation that goes far beyond numbers. It reflects a strategic choice made over decades: investing in renewable sources, expanding the grid, and including the entire population in the national energy system. The integration of Roraima into the SIN was the final chapter of this story of inclusion.

The challenges faced by the solar sector are not signs of failure. They are the problems of a market that grew too quickly for infrastructure and regulation to keep pace. The response is being shaped in Brasília, in transmission auctions, in the regulation of storage, and in negotiations over curtailment compensation.

The Brazil emerging from this cycle is a country that, while confronting its own internal bottlenecks, is already a global benchmark in clean energy. With 84.63% renewables in its energy mix and an expansion plan of nearly 10 GW for the year, the country continues moving in the right direction, even if setbacks along the way are inevitable.

The question is no longer whether Brazil will lead the energy transition. The question is how fast it will accelerate.

{kind=link}