The debate about the future of energy in Brazil often focuses on the expansion of renewable power generation, the strength of the country’s hydropower matrix, the growth of solar and wind energy, and, more recently, the low-carbon hydrogen agenda. This perspective is relevant, but it does not fully capture the complexity of Brazil’s energy transition. There is an equally strategic dimension, often less visible to the general public, involving the use of natural gas and biomethane as vectors for energy security, industrial decarbonization, the replacement of more carbon-intensive fuels, and the economic use of waste.

The article “Gás Natural e Biometano, oportunidades que o país não pode perder”, published by Brasil Energia, draws attention to a central point: Brazil has resources, potential demand, and competitive advantages, but it has still not managed to structure a sufficiently integrated policy to turn natural gas and biomethane into pillars of energy development. The issue is not simply producing more. It is ensuring that production reaches consumers in a competitive, predictable, and environmentally consistent way.

Internationally, natural gas continues to play a relevant role in the energy matrix. According to the International Energy Agency, gas is used in electricity generation, heating, industrial processes, and the production of chemical inputs, while emitting less carbon dioxide during combustion than coal and oil products. At the same time, the IEA itself warns that natural gas remains a fossil fuel and that emissions associated with its value chain, especially methane leaks, must be significantly reduced if international climate goals are to be achieved.

This dual role explains the complexity of the issue. Natural gas cannot be treated as the ultimate solution for decarbonization, but it should not be ignored in countries that need to replace more polluting fuels, ensure flexibility in the power system, reduce dependence on imports, and support industrial activities that are difficult to electrify. In Brazil’s case, this discussion takes on specific contours because the country has a predominantly renewable electricity matrix, but still depends heavily on liquid fuels in transportation, logistics, and parts of industry.

According to the Energy Research Office, Brazil’s energy matrix maintained a renewable share close to 50% in 2025, far above the global average and that of OECD countries. In the electricity matrix, the share of renewables was even higher, led by hydropower, wind, solar, and biomass. This performance, however, does not eliminate the challenges. Energy consumption in transportation grew in 2025, and the sector remains among the main contributors to emissions associated with the national energy matrix.

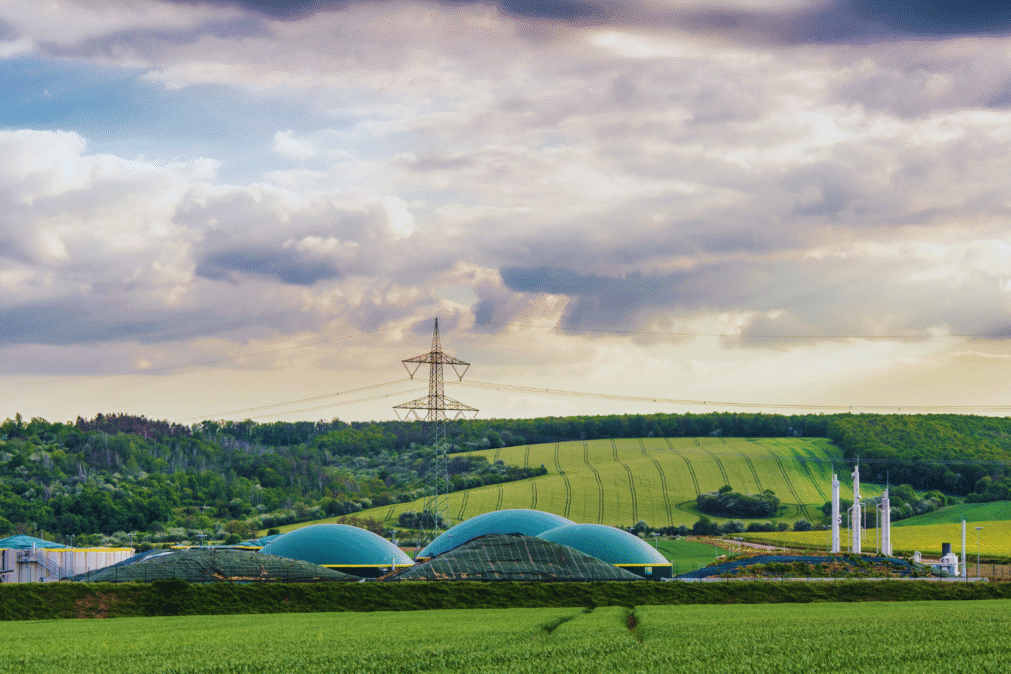

This is where natural gas and biomethane become more strategic. Natural gas can reduce emissions when it replaces diesel, fuel oil, or coal in specific applications. Biomethane, in turn, expands this logic because it is a renewable gas produced from the purification of biogas generated from organic waste, such as vinasse, filter cake, livestock manure, landfill waste, and sanitation effluents. When produced with technical control and traceability, biomethane can replace fossil gas in industrial, vehicle, and thermal uses, while relying on part of the existing infrastructure.

The gap between potential and reality, however, remains wide. ABiogás estimates that Brazil has a theoretical biomethane production potential of around 120 million Nm³ per day, distributed across the sugar-energy, animal protein, agriculture, and sanitation sectors. In a technical document on the mapping of plants through 2032, the association also points to a short-term potential of 34.9 million m³ per day within five years, provided projects move forward. This volume could change the scale of Brazil’s renewable gas market, but it depends on investment, connection to demand, regulatory certainty, and certification mechanisms.

The opportunity is particularly relevant because biomethane addresses energy, environmental, and economic challenges at the same time. In agribusiness, it makes it possible to transform waste into fuel. In sanitation, it creates value from landfills and treatment plants. In heavy transportation, it can replace part of diesel consumption in captive fleets, buses, trucks, and regional logistics operations. In industry, it offers an alternative for consumers that need thermal energy and seek to reduce carbon intensity without relying exclusively on electrification.

This agenda gained new momentum with the Fuel of the Future framework. Law No. 14,993/2024 laid the groundwork for a broader fuel decarbonization policy, including instruments to stimulate biomethane. Later, the Ministry of Mines and Energy announced that the National Energy Policy Council had defined a greenhouse gas emissions reduction target for the natural gas market through the use of biomethane in 2026. The initial target, set at 0.5%, has both symbolic and practical value. It signals the beginning of a regulatory obligation and creates a reference point for economic agents to evaluate projects, contracts, and investments.

Another essential component is the Biomethane Guarantee of Origin Certificate, known as the CGOB. According to the National Agency of Petroleum, Natural Gas and Biofuels, the certificate is intended to ensure traceability for the volume of biomethane produced and traded, certifying characteristics of the production process, the origin of the feedstock, and the production location. This type of instrument is decisive because the low-carbon corporate market requires proof. It is not enough to consume renewable energy or fuel. It is necessary to demonstrate origin, environmental attributes, and compliance.

Traceability will also be important for integrating biomethane into ESG strategies, emissions inventories, decarbonization targets, and, in the future, regulated or voluntary carbon markets. Energy-intensive companies, carriers, retail chains, food industries, logistics operators, and sanitation companies are likely to view biomethane not only as an energy input, but also as part of a strategy to reduce Scope 1 emissions and, depending on the contractual structure, Scope 3 emissions as well.

Despite regulatory progress, physical bottlenecks remain the main obstacle. Brazil produces significant volumes of natural gas, especially in offshore fields, but much of this gas is reinjected into reservoirs for technical, economic, and infrastructure-related reasons. The Brasil Energia article highlights precisely this contradiction: production exceeds effective consumption, but the country is still unable to make all of this resource available to the market under competitive conditions. The concentration of the pipeline network, the distance between producing areas and consumption centers, and the need for new offloading infrastructure limit its use.

In the case of biomethane, infrastructure is also decisive, but the logic is different. Production tends to be more decentralized, close to landfills, sugar-energy plants, agricultural properties, industrial facilities, and treatment stations. This can be an advantage, as it brings supply and demand closer together in certain regions. However, it also creates challenges related to scale, connection, quality standardization, access to distribution networks, and logistical feasibility. In some cases, biomethane can be injected into the gas grid. In others, it can be compressed, liquefied, or consumed locally.

The complementarity between natural gas and biomethane may be the most relevant point in this discussion. It is not a matter of choosing one over the other. Natural gas can provide scale, stability, and supply security. Biomethane can reduce the carbon intensity of the molecule consumed and create a bridge between energy, waste, and the circular economy. In sectors such as heavy transportation, thermal industry, and distributed generation from waste, this combination may be more realistic in the short term than solutions based exclusively on electrification.

In the sugar-energy sector, for example, biomethane production is linked to the availability of crop residues. During periods of greater availability of vinasse and other byproducts, there is greater potential for biogas generation and purification into biomethane. During the off-season, natural gas can act as a complementary source, keeping contracts, infrastructure, and consumers active. This dynamic reduces the risk of discontinuity and improves the economic predictability of projects.

In transportation, the opportunity is significant, but it requires coordination. Gas- or biomethane-powered trucks and buses depend on a reliable fuel supply, fueling stations along the right routes, fleet financing models, and an economic signal in relation to diesel. Without logistics corridors supplied by CNG, LNG, or biomethane, demand will not consolidate. Without demand, investments in production and distribution become less attractive. It is the classic coordination challenge between infrastructure and market development.

Industry can also serve as an important anchor. Many industrial processes require heat, steam, or direct combustion, uses for which replacement by electricity is not always simple or economically viable. For these consumers, gas contracts with a renewable component, backed by certified biomethane, can represent a concrete path toward gradual decarbonization. Regulatory and contractual predictability will be decisive for this market to move forward.

From an environmental standpoint, biomethane has an additional advantage: it avoids emissions that would occur through the decomposition of organic waste. Methane has a much higher global warming potential than carbon dioxide over short-term horizons. Capturing this gas, treating it, and using it as energy reduces emissions and replaces fossil fuels. This double effect explains why biomethane has been gaining ground in climate and energy policies in different countries.

But Brazil must avoid a common trap in transition agendas: turning potential into rhetoric without converting rhetoric into projects. The country has already shown in other value chains, such as ethanol, biodiesel, hydropower, solar, and wind, that it is capable of developing relevant energy markets when public policy, financing, demand, regulation, and business capacity come together. Biomethane needs this same institutional engineering.

There are, therefore, four priority fronts. The first is infrastructure. Without pipelines, local networks, compression and liquefaction bases, storage, and fueling points, the market will not gain scale. The second is regulation. The CGOB, annual targets, certification rules, and the definition of agents’ obligations must be clear, auditable, and enforceable. The third is financing. Biomethane projects require intensive capital, technological risk assessment, long-term contracts, and revenue predictability. The fourth is demand. Without committed industrial consumers, fleet operators, distributors, and corporate buyers, expansion will remain limited.

Brazil’s opportunity is concrete because it combines assets that few countries possess simultaneously: a robust agroindustrial sector, large volumes of organic waste, experience in biofuels, a clean electricity matrix, a relevant consumer market, and the need to reduce dependence on imported diesel. The challenge is to integrate these elements into a coherent energy policy.

The debate about natural gas and biomethane should not be reduced to a dispute between fossil and renewable. The more appropriate question is how to use each molecule more efficiently, with lower carbon intensity, greater supply security, and stronger economic impact. In this sense, biomethane can be Brazil’s differentiator. It transforms waste into energy, brings investments into inland regions, creates new revenue streams for agribusiness, improves the environmental management of landfills and sanitation, and offers a renewable alternative for sectors that will continue to depend on energy molecules for many years.

The country is not starting from scratch. There are already plants in operation, projects under development, interested companies, regulation under construction, and growing corporate demand for traceable low-carbon solutions. What is still missing is speed, coordination, and strategic vision.

If Brazil manages to align natural gas, biomethane, infrastructure, and certification, it could create a more competitive market, less dependent on imports and more aligned with the energy transition. If it fails to do so, it will continue to live with a familiar contradiction: abundant resources, low economic use, and lost industrial opportunities.

The window is open. Biomethane is no longer a peripheral promise and has moved to the center of energy policy. Natural gas, in turn, needs to be treated realistically, as a source of transition, flexibility, and security, but with a commitment to emissions reduction. The combination of the two can represent a pragmatic and competitive Brazilian pathway to decarbonize part of the economy without compromising supply, industry, and logistics.

Brazil has the feedstock, the market, and the technical expertise. The decision now is to turn potential into infrastructure, regulation into trust, and opportunity into long-term energy policy.

{kind=link}